Prepared by Jeanette Rice

Signs are mixed as to the near-term direction of the U.S. economy. There’s no question that 40-year high inflation, higher interest rates and borrowing costs, and declining business confidence are eroding economic expansion, real estate investment activity, and acquisitions pricing. Investment activity has moderated, and cap rates have widened in the past few months.

The challenges of the economy and capital markets environment are mostly all near term. Multifamily’s underlying strengths are keeping the sector on solid footing. Buying activity and investment performance are still near peak levels given their extraordinary upward movement over the past decade. Property fundamentals are healthy and are well positioned to continue to perform favorably.

The longer-term outlook is even stronger given sustained strong multifamily demand. U.S. multifamily housing will continue to provide appealing investment opportunity and returns over the decade to come.

THE U.S. ECONOMY HAS MANY CHALLENGES,

BUT STILL PLENTY OF STRENGTH

Today’s greatest economic challenges are 40-year high inflation rates, high interest rates (double year-ago rates), and declining business confidence. GDP figures were negative for the first two quarters of 2022. However, many economic measures reflect continued strength, most notably employment. The robust labor market should provide the buoyancy needed to keep the U.S. out of recession. That said, national economic expansion will still be modest through the second half of 2022 and into 2023 with the GDP annual growth rates likely staying under 2% over the next few quarters compared to 2021’s 5.7%.

MULTIFAMILY MARKET WELL POSITIONED

TO WEATHER ECONOMIC SLOWDOWN

Despite economic headwinds, multifamily property fundamentals remain favorable and should stay healthy through fall 2022 and into 2023. Unquestionably, market performance has moved downhill from peak Himalayan levels achieved in the past few quarters. But the statistics still reflect superior performance.

- Occupancy was a favorable 96.1% in July according to RealPage, down only one-half percentage point from the prior year.

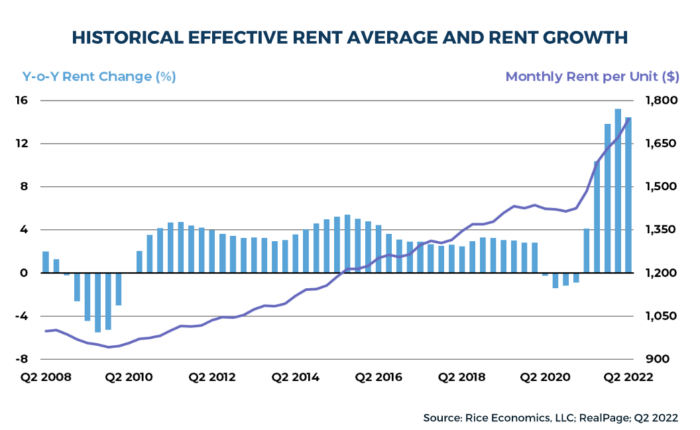

- Effective rent growth was 12.2% year-over-year in July; off from the March peak of 15.7%, but still elevated. (See graph below for long-term historical trend.)

- Rents climbed 0.8% in July alone.

RealPage’s forecasts reflect modest declines in market health, but performance above historical averages.

- Occupancy is expected to stay firm through the balance of 2022 (Q4=96.6%) and then move down one point in 2023 (Q4 2023=95.6%). These rates are still above the historical average of 94.6% (2000 through mid-year 2022).

- Rent growth is projected to stay double digit through 2022, ending the year at 13.2% (Q4 2021 to Q4 2022), and then moderate to 6.3% in 2023. The 2022 forecast is likely overly optimistic, but 2023 probably not. From 2000 through the Q2 2022, annual rent appreciation averaged 3.4% (and 2.8% prior to COVID).

If economic woes worsen and the labor market deteriorates notably, then all of these forecasts are too optimistic. Truly sharp drops in occupancy and rents experienced in earlier recessions are highly unlikely.

MULTIFAMILY DEMAND

POSITIONED TO STAY FIRM OVER THE SHORT TERM

Multifamily demand is high and keeping pace with new supply today. Over the coming months, the industry will be closely watching to see if there’s a pullback in demand. As long as the economy chugs along with modest growth, I expect minimal deterioration, other than typical seasonal patterns (slower leasing in fall and winter).

In past downturns (excluding the very-different 2020 recession), the loss of jobs and income led many renters to double up with family and friends or seek less expensive housing. However, five factors make this time different. These same factors will also help sustain strong multifamily demand long term.

- Renters are older and less inclined than younger renters to move in with roommates and family.

- With work-from-home practices widespread (part time or full time), individuals and families need more space, thereby inhibiting doubling up.

- Rental options are limited today given high occupancy levels, minimizing “flight-from-quality” movement.

- Consumers generally accept the necessity of paying a higher portion of their income on housing.

- Moving from rental tenure to homeownership is highly constrained due to high housing costs; housing has appreciated at a 7.3% annual average over the past 11 years (see graph below), and home affordability today is at its lowest level since June 1989.

DEVELOPMENT ACTIVITY IS HIGH,

NOT LIKELY TO SHIFT SUPPLYDEMAND BALANCE

Multifamily development activity is at the highest level since the mid-1980s. Construction starts through July totaled 306,900 units, up 18% from the same period last year. The seasonally adjusted annual rate for 2022 is running at 529,300 units, the highest level since 1986 as shown on the chart below.

In past periods of economic slowdowns, high levels of new supply contributed significantly to market deterioration. Today’s market conditions are different; market demand is expected to hold up quite well. There will be submarket pockets where new supply exceeds demand in the short term resulting in slower lease-ups and reduced effective rents. However, broadly speaking, most of the new supply being delivered in the near term should be readily absorbed due to housing demand.

MULTIFAMILY INVESTORS TAKING A

COFFEE BREAK

The multifamily capital markets environment has cooled this summer, but only from recent record-breaking investment and pricing levels. The investment appetite for multifamily product remains keen. Investors are still achieving solid returns. Although negotiations may be more protracted, buyers and sellers are still finding deal opportunities.

H1 2022 multifamily investment was impressive especially when compared to 2021’s record-breaking activity. H1 2022 totaled $154.6 billion according to MSCI Real Capital Analytics, up 53.1% year-over-year. Among different property types, multifamily had the largest market share by far in H1 with 41.1% of total investment.

Higher interest rates and higher borrowing costs began to slow investment activity beginning in Q2 despite sustained strong market fundamentals. The cooler investment climate has created some uncertainty and decline in value. Less capital flowing into the sector combined with higher interest rates also have led to cap rate expansion in recent months, on average of around 50 bps.

Borrowing costs have jumped and terms have tightened. In August 2021, CBRE Capital Markets cited typical agency borrowing costs in the low to mid 3%s for 10-year fixed-rate loans at 60% to 65% LTV. As of mid-August, agency debt was around the mid to high 4%s and DSCRs had climbed to 1.25 minimum. Borrowing costs from higher-leverage lenders like the debt funds have risen even more over the past few months.

Bid-ask gaps have become more common. Some prospective buyers have moved to the sidelines temporarily; many owners are deferring putting assets on the market. The whole multifamily world is watching how cap rates, spreads, and acquisition pricing will trend in the coming months. Pricing uncertainty will continue as long as the Fed keeps raising rates; once that’s off the table, the multifamily marketplace should see renewed vigor.

OWNERS, BUYERS AND SELLERS ARE

FINDING SILVER LININGS IN CURRENT

CAPITAL MARKETS CLIMATE

Even with nervousness in the capital markets environment, there is still plenty of activity today. With a less-competitive marketplace, many prospective buyers are finding buying opportunities not previously available. Most multifamily buyers active in early 2022 are still in the market or at least kicking the tires, offering sales potential to owners ready to sell. Multifamily remains liquid, even if pricing is off peak.

Market players that take a more historical view of the capital markets – rather than just comparing the current investment climate with just the red-hot 2021-early 2022 period – continue to see a favorable environment.

- Apartment communities acquired almost anytime within the last decade experienced tremendous appreciation during the holding period and have significant embedded gains. If sold today, even with pricing off the early-2022

peak, sellers can reap attractive rewards. - Borrowing costs are clearly higher today than in recent history, but they are still not anywhere near approaching historical highs, and especially so for lower-leverage deals.

- The abundance of multifamily lenders and their need to place debt capital will keep lenders active and motivate them to become more competitive in coming months.

CAPITAL FLOWS INTO THE

MULTIFAMILY SECTOR TO REMAIN HIGH

Total 2022 multifamily investment will end up perhaps 20% down from the sky high 2021 level, but still come in as the second highest year since 2001 when MSCI Real Capital Analytics started collecting sales data. Cap rates may widen further in H2 2022 but still remain very low on an historical basis.

In addition to the specific strengths of the multifamily market, capital flows into the sector will stay relatively high for three reasons.

- The multifamily sector is attractive for both cash flow and for appreciation. While appreciation will stay muted near term, the sector continues to shine for its cashflow characteristics.

- For multi-asset class investors, real estate is generally a better bet given higher inflation (partly because new leases can absorb much of inflation’s impact).

- Within commercial real estate, multifamily and industrial are favored classes, a status unlikely to change any time soon. Office is surrounded by lack of clarity on the future of work and its impact on office demand. Retail is recovering from 2020, but its on-going structural shift to ecommerce makes choosing the right retail assets tricky. Many real estate “alternatives” (life sciences, self storage, data centers, etc.) are appealing due to their favorable structural drivers, but most are too small for large-scale investment and/or too specialized for most investors.

MULTIFAMILY TO WEATHER THE

STORM WELL AND REMAIN HIGHLY

APPEALING LONG TERM

The U.S. economy may be headed into rougher waters. Higher interest rates have slowed investment activity and widened cap rates modestly. Double-digit rent increases and tight occupancy rates from early 2022 are moderating. Yet multifamily property fundamentals remain at healthy levels. Investment remains active and property values remain near their historical highs. The multifamily market is positioned to perform well over the long term given strong demand drivers, including expensive housing costs which keep renters from moving into homeownership. Multifamily will remain a very appealing investment product for the long term.

The Article Author

Jeanette I. Rice, CRE

Rice Economics, LLC.

Ms. Rice is one of the country’s leading multifamily economists. She is the founder of Rice Economics, LLC, a consulting firm providing real estate economics and business consulting for commercial real estate firms.

Prior to Rice Economics, LLC, Ms. Rice was Americas Head of Multifamily Research for CBRE, the largest multifamily debt and equity intermediary in the U.S. At CBRE, Ms. Rice covered nearly all aspects of the U.S. multifamily property and capital markets. She was a frequent speaker at industry events and wrote hundreds of white papers and research briefs on the sector. Her more notable white papers included: The Case for Workforce Housing; The Single-Family Built-to-Rent Housing Sector; The Way Forward – Path to Urban Multifamily Recovery; Global Outlook 2030 – Multifamily; and U.S. Multifamily Primer for Offshore Investors.

Ms. Rice began her career in the multifamily sector. One of her first positions was with Embrey Investments where she conducted feasibility analysis for prospective developments and provided investment strategies for Embrey’s geographic expansion in the 1980s. Following Embrey, Ms. Rice held research leadership positions with HFF (now part of JLL), Lend Lease Real Estate Investments, Crescent Real Estate Equities, and Verde Realty.

Ms. Rice has been involved with many professional organizations through her 40-year career. In particular, she has been active with the National Multifamily Housing Council for many years. She is a Counselor of Real Estate and has held numerous leadership positions with the Counselors of Real Estate organization. Ms. Rice currently serves on the TCU Center for Real Estate Executive Council.

Ms. Rice earned a B.A. in history from the University of Washington and M.A. in urban geography from Queen’s University in Canada. She also completed two years of graduate coursework in urban geography at The University of Chicago. Ms. Rice is a 40-year Texas resident, currently based in Fort Worth.

About Embrey

Embrey is a fully integrated real estate investment, acquisition, development, construction and management firm focused on creating maximum value for our partners. Embrey’s strong performance over nearly half a century demonstrates the value created by disciplined investing and a keen eye for detail.